Indirect Costs at NIH . . .

I wasn’t planning on spending part of a Saturday writing about cost accounting principles and the like, but NIH-world was hit with a doozy of a policy announcement on Friday night:

Immediate reduction of indirect cost rates to 15% for all NIH grants:

The solitary rationale offered in the official notice: foundations do it.

Most private foundations that fund research provide substantially lower indirect costs than the federal government, and universities readily accept grants from these foundations. For example, a recent study found that the most common rate of indirect rate reimbursement by foundations was 0%, meaning many foundations do not fund indirect costs whatsoever. In addition, many of the nation’s largest funders of research—such as the Bill and Melinda Gates Foundation—have a maximum indirect rate of 15%. And in the case of the Gates Foundation, the maximum indirect costs rate is 10% for institutions of higher education.

Of course, the only reason universities begrudgingly accept such low indirect rates from philanthropy is that it’s an exception, and they don’t have to accept such low rates from federal grants. But in any event . . .

There’s just one problem

In several appropriations bills (including the most recent one from 2024), Congress specifically banned NIH from doing anything to change how indirect costs are determined.

That is, the federal rules on indirect costs apply to NIH as determined in mid-2017 (you might remember that mid-2017 is exactly the time when the previous Trump administration unsuccessfully tried to limit indirect costs to 10%). Moreover, no funds given to HHS can “develop or implement a modified approach to such provisions.”

This is about as open-and-shut as it gets. If the NIH announcement is challenged in court, I am 99.9% confident that it will immediately be overturned.

Someone might point out that the NIH’s official notice purports to rely on section 75.414(c) of 45 C.F.R., which does seem to allow HHS’s divisions to change indirect costs.

But not so fast. Note how limited the language actually is:

The negotiated rates must be accepted by all Federal awarding agencies. An HHS awarding agency may use a rate different from the negotiated rate for a class of Federal awards or a single Federal award only when required by Federal statute or regulation, or when approved by a Federal awarding agency head or delegate based on documented justification as described in paragraph (c)(3) of this section.

So, an HHS division like NIH can use a different rate only for a “class” of grants or a “single” grant, and only with “documented justification.”

There is nothing that says NIH could, in one fell swoop, overturn literally every negotiated rate agreement for 100% of all grants with all medical and academic institutions in the world, with the only justification being “foundations do it” rather than any costing principle whatsoever from the rest of Part 75 of 45 C.F.R.

In any event, NIH’s purported justification for reducing indirect costs can’t override the fact that Congress specifically banned NIH from doing any such thing.

What Should Happen Going Forward?

The current attempt to change indirect rates is entirely unlawful, but a future Congress could still empower HHS/NIH to reduce indirect rates in a more thoughtful way.

What’s the right answer here?

A few observations:

First, anyone who wants to get up to speed on indirect rate calculations should read Kelvin Droegemeier’s 2017 testimony here. The history section is particularly fascinating. None other than Vannevar Bush pioneered indirect cost reimbursement during World War II at a flat rate of 50%, since that was “one-half of the 100% being charged at that time by industrial contractors”!

Moreover, federal reimbursement of indirect costs was seen as a way to get universities to accept federal funding at all, since at the time many universities “had no interest” in federal funding “owing to fears about government intrusion in curricula, research topics, and governance.”

My, how the world has changed . . .

Second, as Droegemeier points out, the post-World-War-II era saw dramatic changes here: “The grant indirect cost limit was set at 8% in 1950, then revised to 15% in 1958, and then raised to 20% in 1963 and extended to grants awarded by all other agencies.”

But there’s probably a good reason that indirect cost rates have risen steadily since then. While 65-70% may be far too high, I’m not aware of any actual organization or company that operates with a true indirect rate of 15%. Consider Microsoft’s latest 10K:

As a rough analogy to universities, we could assume that cost of revenue ($74,114) plus sales ($24,456) are equivalent to direct costs attributable to some specific product on the market right now, while R&D and general/administrative are more like indirect costs. In that case, Microsoft’s indirect rate is 37.7%. That’s just a rough estimate, of course, but the point is that even private profit-seeking companies do see a need to spend a lot of money on facilities, personnel, and activities that aren’t directly tied to a specific income stream.

Third, there’s a lot of administrative bloat at universities, and I (like many others) can see a case for limiting indirect costs to, say, 50% at maximum as a way of forcing more efficiency.

But if we want to reduce indirect costs more seriously, we also need to reduce the federal regulatory burden that causes universities to hire so many administrators in the first place.

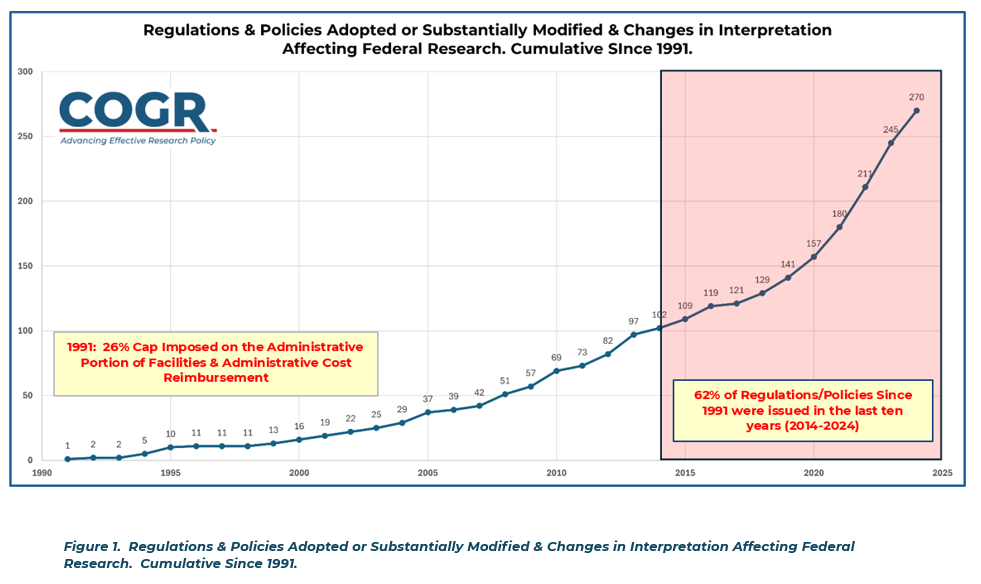

Consider COGR’s painstaking effort to track the federal regulatory burden over the past few decades. It’s a 13-page table tracking about 270 regulations:

Put another way:

Imagine if we could get back to the regulatory burden of the year 2000. I’m old enough to remember the year 2000, and while I wasn’t paying close attention to the R&D enterprise at the time, it seemed to work just fine. NIH made grants, professors did biomedical research, and the world wasn’t falling apart such that we would have all died without 250 new regulations.

If Congress, the White House, and HHS delved into these 270 regulations, and came up with a plan for prioritizing which ones to keep, which ones to modify, and which 200+ to eliminate altogether . . . well, then we would be much better positioned to say that universities should have to live with a highly-reduced indirect cost rate. Less regulation and lower indirect costs—a win-win!

Of course, the whole effort would be incredibly tedious, and you’d need to involve subject-matter experts rather than just people who are good at computers but don’t know anything about government, science, or universities.

But that would be the most promising way of improving efficiency in research. Trying to cut indirect costs unlawfully without cutting the regulatory burden is a dead end.

***

PS: In unrelated news, Johns Hopkins University just announced the winners of a science journalism fellowship that Good Science Project sponsored (albeit with no editorial input on our side). Looking forward to these projects!

Thanks for an excellent article on this - so many of the articles coming out don't really understand IDC. Two caveats, however:

1. When computing F&A rates, the federal government caps the portion for administration at 26% - no matter how much regulatory burden the government places on universities and how much administrative bloat Universities would like to fund from F&A, they can only justify 26% as administrative costs. Most Universities (including mine) are at this administrative cap. The different between 26% and the University's F&A rate can only be due to facilities costs.

2. Universities could change how they account for a portion of their indirect costs to account for them as direct costs. Doing so would be a good way to reduce IDC rates and increase transparency to agencies on where their fudns are going, but developing these cost models and accounting mechanisms takes time. For example, computer security compliance costs have typically been funded as indirect costs (and they're administrative and so are capped), but the recent DOD CMMC guidance allows Universities to direct charge for them. Most every University is still figuring out how to do so in a way that both makes sense and meets federal regulations.

This is an excellent post, and I endorse your proposals. But IDC rates in the 80s were higher than now even though they had far less annoying regulations then.

My favorite example is when Stanford used 200K of IDC money to refurbish a yacht.

https://web.stanford.edu/dept/pres-provost/president/speeches/941018indirect.html