Federal Indirect Costs--Does a Flat Rate Make Sense?

Whatever happens with the court case as to NIH’s initial attempt to limit all indirect costs to a flat rate of 15%, virtually no one thinks that indirect cost calculations are going to stay the same going forward.

What if the federal government attempts to use more appropriate mechanisms to impose the same flat rate of 15% (or perhaps another rate such as 25%)? Nearly everyone expects something like this to happen eventually.

TL;DR Indirect cost reform seems long overdue. Costs are likely too high and are not transparent at all. But a flat rate makes no sense. We should move forward by taking actual costs into account and mandating transparency, while incentivizing greater efficiency coupled with deregulation of the many burdens imposed on universities.

Several thoughts on indirect costs

Imposing a flat rate would require significant changes (if not near abolition) of current regulations.

Specifically, Appendix III to 2 CFR Part 200, which describes how institutions of higher education are supposed to tally up their indirect costs when negotiating a rate with the federal government.

Right now, universities are allowed to include the following, which are obviously tailored to their own actual costs:

Costs (including depreciation) for buildings, capital improvements, and equipment (if buildings are used for more than one function, then the university has to break that down by square footage or by the proportion of employee salaries who use that space)

Interest on debt associated with buildings and equipment (again, broken down by different functions)

Operation and maintenance expenses, which include:

Repairs

Furniture

Maintenance of buildings

Security

Disaster preparedness

Environmental safety

Hazardous waste disposal

Insurance

Central receiving

Utilities

[PS, note that some of the above are mandated by federal law, state law, or both]

General Administration, including

Executive and administrative functions that aren’t solely about instruction or other research activities (it can include central offices such as the President, Chancellor, institution-wide financial management or safety/risk management, and so forth)

Departmental Administration, including:

academic deans

central departmental functions like secretarial staff

office supplies, stockrooms, etc.

Sponsored Projects, including:

Grant and contract administration

Purchasing

Editing and publishing

Library expenses (including salaries and the cost of books and journals)

Student Administration, including:

Dean of students

Admissions

Registrar

Counseling and placement services

Student advisers

Student health services

OK, that’s a lot! On to the next point:

It’s a false distinction to say that direct costs go to “the research” and indirect costs are going to something other than research.

Many indirect costs (not all—see below!) are a necessary part of research.

Imagine going to a restaurant and expecting to see an itemized bill breaking down exactly much you paid for the following:

The specific ingredients used in your meal

Salaries for the time spent by the cook and the waiter

Salaries for the 1-2 minutes spent clearing the table and washing dishes

The prorated portion of rent considering the size of the table you occupied and for how long

The prorated portion of the electricity, gas, and water used to produce your meal

The prorated cost for cleaning the entire restaurant at night

The prorated cost of all levels of management (the assistant manager, the full manager, and any costs due to overall corporate management)

The prorated cost of any legal and accounting expenses due to your meal

The prorated cost of buying refrigerators, ovens, utensils, cooking supplies, menus, uniforms, light bulbs, signage, etc.

Now imagine trying to demand that you’re basically only going to pay for the first 3 items on the list. All the rest are indirect costs, and you will only pay the bare minimum for those.

Well . . . good luck finding a restaurant if no one wants to pay for all of those expenses! Restaurants wouldn’t exist if the only thing they could pay for were ingredients, cooks and waiters, and washing up. You still need a building, electricity, gas, water, refrigerators, ovens, management, accounting and payroll, and so forth.

Without all of that, there is no restaurant—and no meal.

The same is true for universities and academic hospitals, etc. Without dozens of expenses that are part of indirect costs, no research would occur at all.

That’s why the NIH’s announcement in February was not quite right. It said, “It is accordingly vital to ensure that as many funds as possible go towards direct scientific research costs rather than administrative overhead.”

Sure, all else equal, we shoud make sure that overhead is minimized . . . but, without administrative overhead, the direct research wouldn’t occur at all, especially given the burden of several hundred federal regulations!

Indirect costs are arguably a distraction.

When you buy a meal at a restaurant, you really just care about the overall expense versus the overall experience (taste, atmosphere, service, etc.). If you had a great meal at a decent price, why would you care whether 10 cents or 20 cents went towards filing the restaurant’s annual tax return?

The same is true for research. What we should care about for every research project is whether the expected results are worth the overall cost, not how the overall cost was divvied up internally at the research institution.

If someone comes up with a treatment that helps Parkinson’s disease, the last thing I would say is this:

“Wait, before I get too happy about being able to address Parkinson’s, I have one key question: out of the $1 million grant, was $10,000 or $12,000 allocated towards the lab’s janitorial services over the previous three years? I would rather not have a cure for Parkinson’s than have to live with the knowledge that a university’s internal cost accounting put a little too much towards a category labeled ‘indirect’!”

Flat rates make little sense, no matter what the rate might be (whether 15% or 50%).

Imagine trying to demand that every single restaurant where you eat has to spend 15% on those costs—no matter whether they’re a suburban McDonald’s, a food truck in Manhattan, or the Old Ebbitt Grill in DC. That would not be sensible. Obviously, all of those restaurants have different expenses for rent, management, equipment, and so forth.

The same is true for universities and academic medical centers, etc. A university that happens to do mostly computational social science will have a lower indirect cost rate than a university with a large medical school and an electron microscope.

Or to take an extreme example, the University of California system operates the only university-based particle accelerator in the United States, along with a wide range of highly expensive facilities covering nanoscience, energy, and other fields. What they spend on buildings and equipment is obviously not the same as at the University of Central Arkansas (in my home state).

Expecting the indirect cost rate to be the same at Berkeley as at regional universities is like expecting to pay the same for a New York food truck as for an 8-ounce wagyu steak at Bourbon Steakhouse in Washington, DC.

You’re not buying the same thing at all. You can’t expect the costs (direct or indirect) to be the same.

Fifth, almost no one in this debate seems to fully grasp how indirect costs are actually calculated.

As a reminder: if an indirect cost rate is 50%, that does NOT mean that 50% of our funding is going towards indirect costs. Instead, it means that the indirect costs are 50% of the direct costs.

Simplified example: If we give a $100 grant to a university with a 50% indirect cost rate, $100 goes to the researcher’s lab, and an extra $50 goes to the university.

Total cost: $150.

So out of that $150, the $50 in indirect costs is actually just 33% or 1/3rd.

[The way we talk about indirect costs is almost guaranteed to mislead people into thinking that we’re spending way too much!]

Moreover, almost no one seems to know that universities’ indirect cost rates are subject to so many exceptions that the true rate is actually far lower. For example, Harvard’s top indirect rate is a jaw-dropping 69%.

That sounds extortionary, especially at Harvard (endowment: $50 billion).

But Harvard doesn’t actually get anywhere near 69%.

Instead, if you look at Harvard’s actual agreement with the federal government, the allowable costs exclude:

capital expenditures (buildings, renovations, and individual items of equipment),

costs of patient care (this is huge for Harvard, because it performs so many clinical trials where patient care is the major expense), and

graduate student tuition, stipends, and fellowships.

What are universities actually receiving in indirect costs?

A forthcoming paper from Pierre Azoulay (MIT), Daniel Gross (Duke), and Bhaven Sampat (ASU) gives an answer. They drew on data (often gotten with several years’ effort via FOIA) for 354 NIH-funded institutions that represented about 85-90% of NIH expenditures between 2005 and 2024. It was a truly heroic effort to aggregate data from many different sources.

The result:

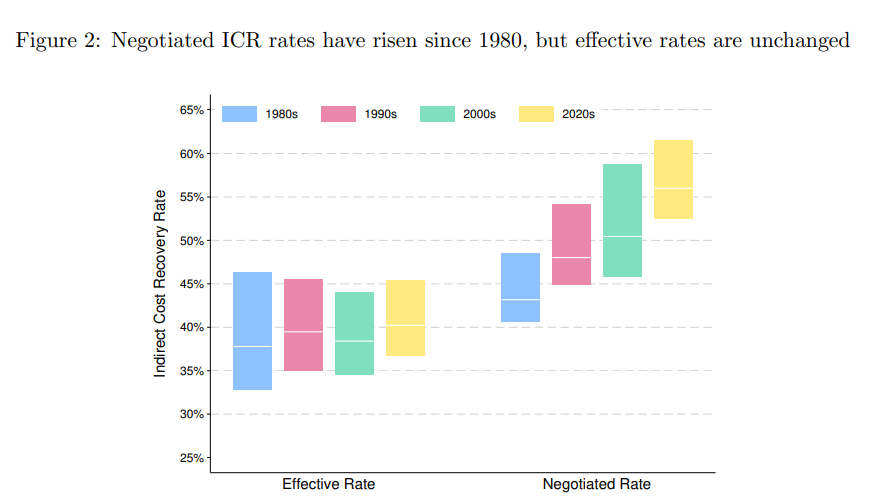

“Whereas most institutions’ negotiated F&A rates are between 50% and 70%, effective rates in practice are generally between 25% and 45%.”

As you can see, the actual indirect cost recovery is far lower than the advertised rates: most institutions are around 40%. And given the point I made above, a 40% indirect cost rate would mean this:

If we give $100 to a university research, an additional $40 would be for indirect costs. That means $40 out of $140, or 29%.

That doesn’t seem too unreasonable, eh? When you eat at a restaurant, do you get upset if “only” 71% of the cost of your restaurant meal went towards ingredients and cooking, while 29% went towards rent, gas, electricity, refrigeration, and the management? Indeed, why would you spend one second worrying about that if you enjoyed the meal?

Another interesting finding is that even though the “official” negotiated rates have risen in the past 50 years, the effective rates have remained the same!

Again, that’s because the actual rate paid can be far different from the “on-paper” negotiated rate, depending on how many exceptions there are.

Worth keeping in mind is that an indirect cost rate cap (or a flat rate) would hit independent hospitals and research institutions the hardest. They don’t have students (tuition) and alumni donations to draw upon, and their indirect cost rates are always the highest. Thus, any attempt to lower indirect cost rates “will be largest for independent research hospitals (such as St. Jude Children’s Research Hospital in Memphis, TN) and non-profit institutes (such as Cold Spring Harbor Laboratory on Long Island, NY).”

Finally, there is still quite a bit of room for indirect cost reform.

For one thing, universities are completely opaque as to their actual cost structure. We could expect more transparency here.

For another thing, it isn’t clear that the list of indirect costs in 2 CFR is ideal.

Why we should include Student Administration costs (including even the registrar!) in the official list of covered indirect costs? Why aren’t those covered by tuition?

And why are we covering so many building-related costs? It makes to pay for buildings to some extent, but what if we’re incentivizing over-building? (See this short article by the eminent Bruce Alberts: “Overbuilding Research Capacity.”) Plus, many buildings are paid for, in theory, by alumni or rich donors who want their name on the front—are we inadvertently paying for those building expenses after the fact?

It is absolutely worth questioning whether and how we pay for these and other expenses, or whether we want to impose some reasonable cap to incentivize efficiency.

My main point is that a flat rate doesn’t address the real issues here. Some organizations actually do have way more expenses for buildings and equipment than others. There’s no reason to pay them all the same.

I've been reading all your posts on Indirect Costs and there are some interesting ideas and insights. I take issue with one of your first sentences "[c]osts are likely too high and are not transparent at all." This seems like a talking point I keep seeing over and over. Based on what I know from 16 years of experience in research administration (full disclosure: I am not an expert in how the indirect sausage is exactly made), it seems that the calculation that goes into indirect rates is fairly precise but very bureaucratic involving the need to hire "consultants". The amount of time we waste on building and space classification (bean counting), for example, is absurd. I do not think that rates are somehow gamed in ways that create largesse, nor in real dollars does it significantly result in unchecked waste. It's not the rates that are exactly problematic as everyone seems to be fixed on.

The real issue here is government regulation - and I say this as a liberal. There are two key things going on here: one, administration of grants has had very little innovation since I started in the late 2000s. Yes, universities have purchased systems that are slightly more efficient at transmitting proposals to agencies, but on the post award side where we spend most of our time, we still manage complicated effort and large budgets on excel spreadsheets. I know there are tech companies that are earnestly trying to solve some of these massive inefficiencies - the computing power and technology are there, but the biggest factor is university adoption of such systems. They don't want a third party to have a connection to their data warehouses for security reasons. This makes the risk assessment and procurement process next to impossible for deploying technology that could drastically reduce complexity and administrative burden.

The second issue is the Federal government. You posted a COGR graph showing the regulatory burden that has exploded since Uniform Guidance went into effect in 2014. In my lived experience I can tell you that my work life has gotten increasingly worse since UG. Anyone that has had to manage a faculty members’ effort over the salary cap on 16 projects knows exactly what I'm talking about. The way grant effort is tracked and reported is insane. Procurement is another area, as is the lack of uniformity in post award actions at the sponsor level from how we request prior approval, the forms we use, the lack of clear guidance, etc, etc.

I think when people bring up efficiency, they are talking about administration, but many don’t understand that administration costs are capped at 26% (and have been since the 90’s). The “Administration” part of F&A is almost never fully recovered by institutions and is often a loss leader, so anything over 26% is really on the university (not taxpayers) and if they were smart and efficient they would get their admin costs closer to 26%. The Facilities part of an F&A rate are really the driver here. Because of this Universities are in some ways incentivized to grow and expand their campus footprint (as also pointed out), but to what extent I'm not sure. So, when people say things like incentivize efficiency, it sounds good, I just don't know how you operationalize that in terms of the actual rate agreement if we're talking about space being the main driver.

The real question I don't think is about indirect costs per se and whether the rates are “too high”- indirects are a laughably small portion of grant costs on a macro level and related to the federal budget. If you do the budget math for NIH, indirects work out to 20% of the proportion, with 80% to directs. I do wonder if we could get to a flat rate or a tiered flat rate that just treats all projects the same and gets rid of MTDC and everything that is administratively burdensome about having to justify rates in the first place. Universities would save loads of time if we stopped accounting for all our space. It would make training grants, for example less of a money pit and ultimately allow everyone to focus on more important things like actually doing and supporting research. Certainly, this could be modeled at a large scale to get an answer on the best approach.

I think we are saying much of the same thing, just slightly different. I would be interested in actual models to show if you could get to a lower effective, flat rate with significantly less burden involved.

I'm not entirely convinced by this. One of the main problems with the current system is that it incentivizes inefficiency and disincentivizes efficiency. If a university makes its operations more efficient, then it gets less money from the federal government. I've seen this have real consequences for how universities think about investments and return on investment (e.g., expenditures that would come out of their own budget, which reduce their ongoing operating costs).

I think a flat rate (which would be around 50%, not 25% or 15%) would make sense. Note that cost of living, which you raise as a disparity between different institutions, is already part of direct costs -- if the indirect costs in an expensive urban area are higher, well, so are the direct costs, so the ratio should be similar. And, if the UC system has a particle accelerator, and we think that's a good thing, why should sociology grants be paying part of the cost of that? If that is actually worth having, there are probably better ways to pay for it!